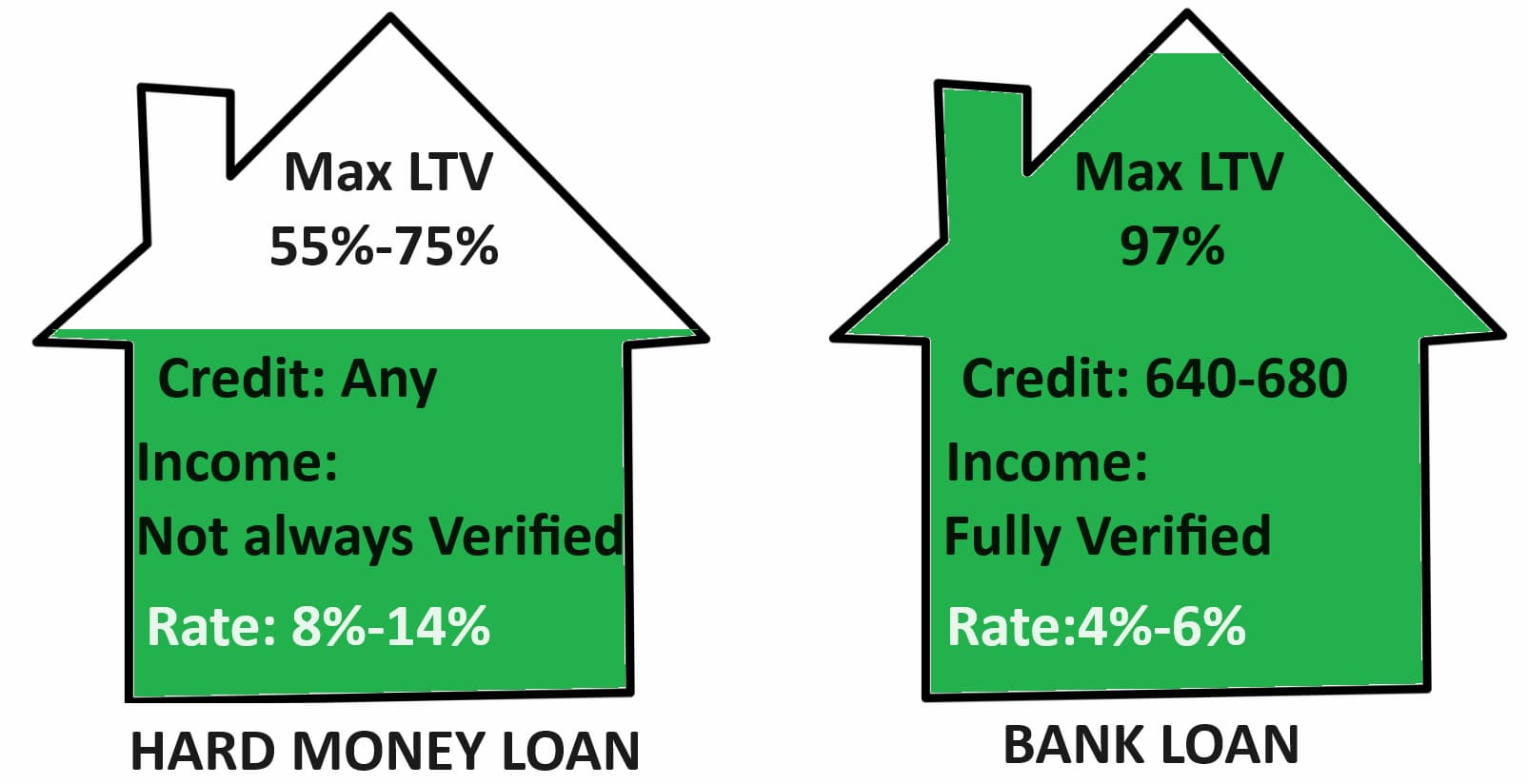

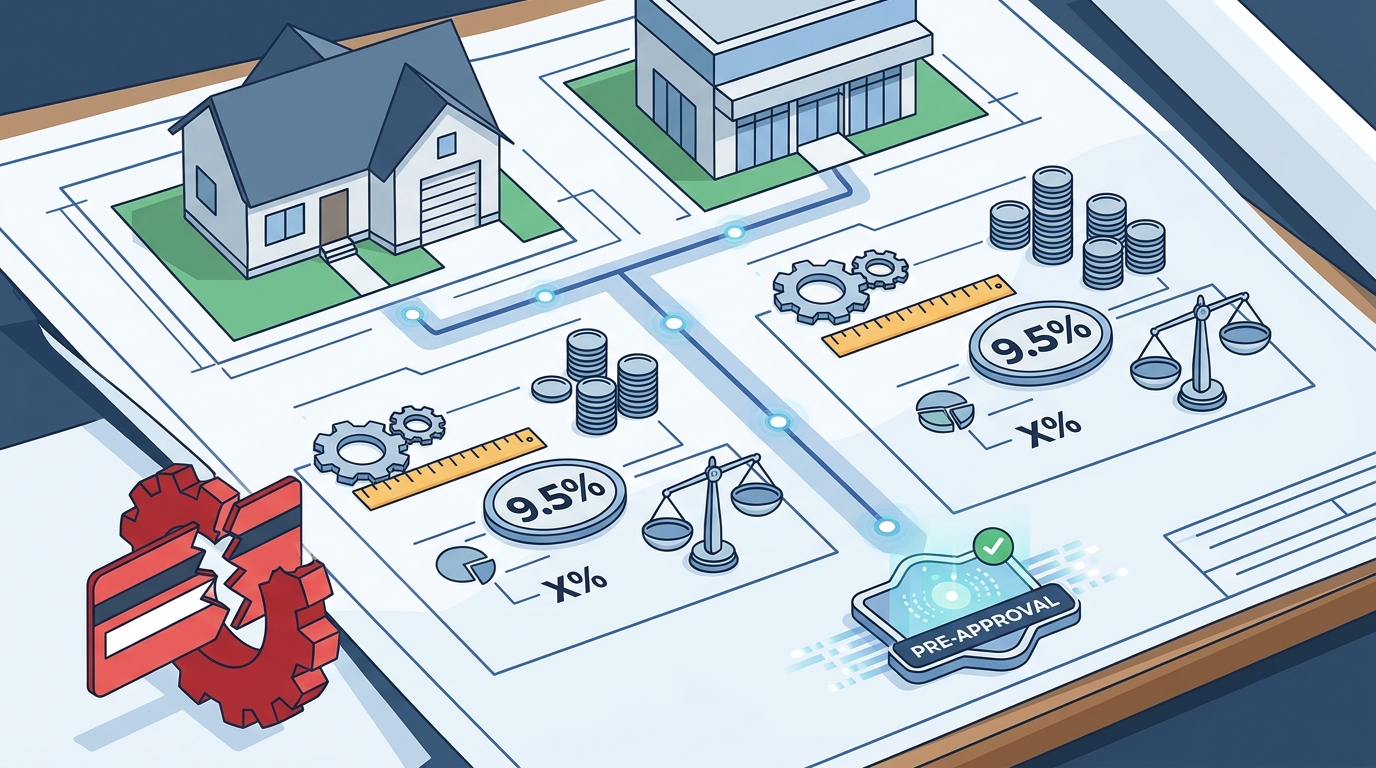

Securing a hard money loan requires understanding a completely different framework than traditional bank financing. Rather than focusing primarily on personal income, private lenders prioritize the asset. This comprehensive guide breaks down the "5 Master Factors" determining your hard money rates and origination fees.

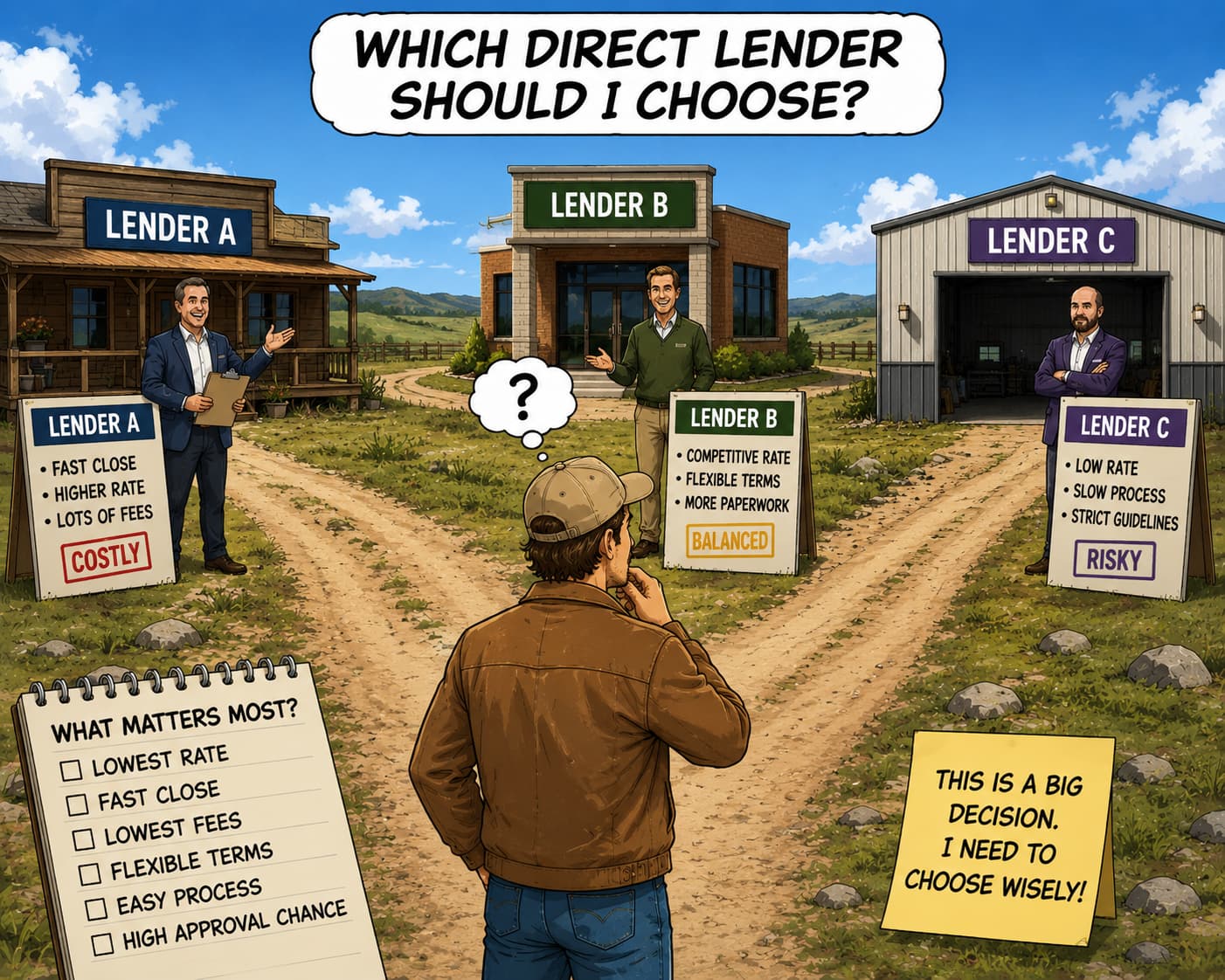

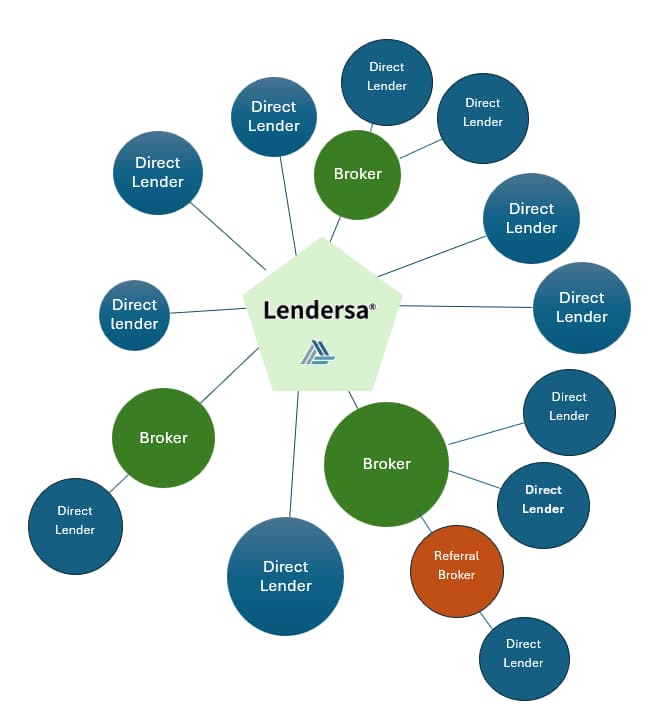

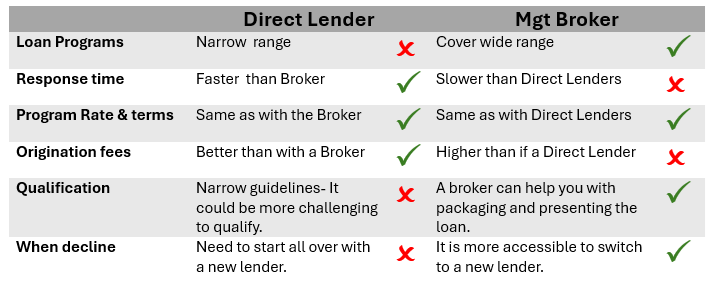

It begins with Property Factors, highlighting how Loan-to-Value (LTV) reigns supreme, alongside property type, condition, and income. Next, it explores Borrower Factors, noting that while credit matters, an investor's track record and exit strategy carry more weight. The guide also details essential Loan Features like duration, prepayment penalties, and funding speed, before examining the motivations behind The Lender ecosystem (local vs. national, brokers vs. direct lenders). Finally, it addresses macro Market Influences, such as local real estate trends and economic shifts.

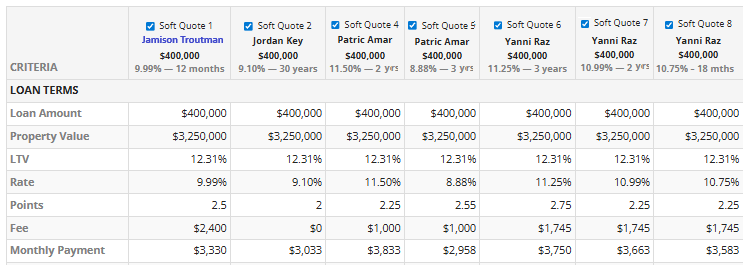

Ultimately, while baseline national averages provide a starting point, completing a customized loan scenario is th