Non-Recourse Commercial Real Estate Loan Documents: What You Need Organized by Category

Non-recourse commercial real estate loans shield your personal assets

from lender claims if the deal goes south—but that protection comes at a

cost: a thick, precisely assembled document package. Unlike a standard

recourse loan where your personal guarantee backstops everything, a

non-recourse structure forces the lender to rely entirely on the

property and the borrowing entity. That means every piece of paper you

submit serves a specific risk-mitigation purpose.

This guide organizes every required document into four functional categories—Entity & Legal Structure, Property & Asset, Sponsor & Financial, and Closing & Post-Closing—so you can see why each document matters, not just that it is needed.

Why Non-Recourse Loans Demand More Paperwork

In

a recourse loan, a personal guarantee gives the lender a fallback: if

the property cannot cover the debt, they can pursue your bank accounts,

other properties, and wages. A non-recourse loan eliminates that

fallback. The lender's only avenue for repayment is the collateral

property itself and the income it generates.

Because lenders

absorb more risk, they compensate by scrutinizing every dimension of the

deal. Eligibility requirements are stricter—typically requiring Class A

or strong Class B assets, a minimum debt service coverage ratio (DSCR)

of 1.25x, and loan-to-value (LTV) ratios between 65% and 75%. The

documentation package is the mechanism through which the lender verifies

every one of these thresholds.

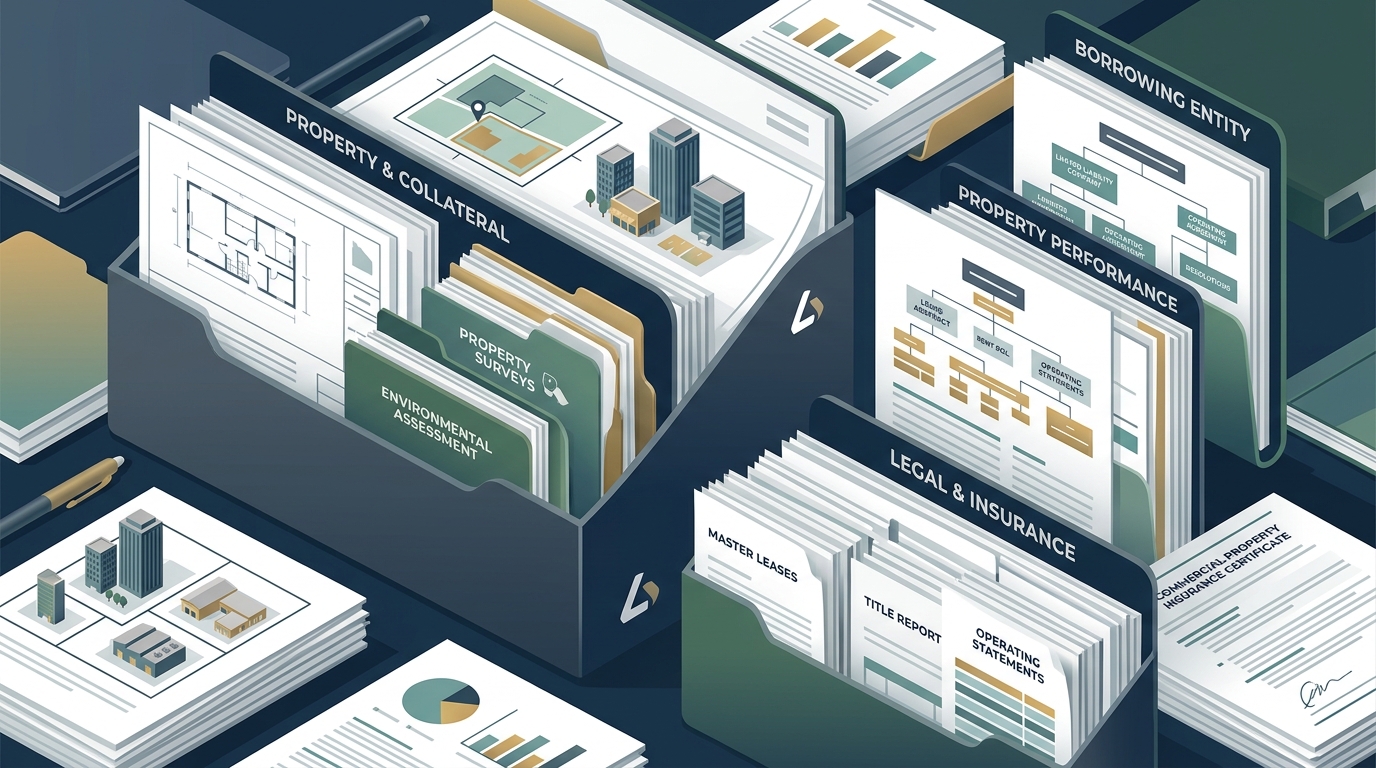

Category 1 — Entity & Legal Structure Documents

Non-recourse lenders almost universally require the loan to be held inside a Single Purpose Entity (SPE).

The SPE exists for one reason: to own the collateral property and

nothing else. This structure isolates the asset so that other business

liabilities cannot drag the property into an unrelated bankruptcy.

1. SPE Formation Documents

You

will submit the articles of organization (for an LLC) or certificate of

incorporation, along with the operating agreement or bylaws. Lenders

review these for bankruptcy-remote provisions—clauses requiring

unanimous consent, including from an independent director or manager,

before the entity can file for bankruptcy or dissolve.

2. Certificate of Good Standing

A

recent certificate from the state where the entity is formed proves the

SPE is active, compliant with state requirements, and authorized to

transact business.

3. Borrowing Entity Resolution

A formal

resolution from the SPE's members or board authorizing the entity to

enter into the loan, pledge the property as collateral, and designate

signatories.

4. Organizational Chart

A diagram showing

every entity and individual in the ownership chain—from the SPE at the

bottom to the ultimate beneficial owners at the top. Lenders use this to

identify related-party risks and ensure there are no undisclosed

affiliates.

Category 2 — Property & Asset Documents

Since

the property is the lender's sole recourse, they need to understand

every physical, legal, and financial attribute of the asset. This

category is the heaviest in terms of volume.

5. Commercial Appraisal

A

full appraisal conducted by a licensed MAI appraiser establishes market

value. Non-recourse lenders typically cap LTV at 65–75%, so the

appraisal directly determines how much you can borrow.

6. Rent Roll

A

current rent roll lists every tenant, their lease start and end dates,

monthly rent, any concessions, and security deposits held. Lenders use

this to model the property's cash flow and calculate DSCR.

7. Historical Operating Statements (Trailing 12 and 3-Year)

Profit

and loss statements for the most recent 12 months and the prior two to

three years demonstrate the property's income trend. Lenders

cross-reference these against the rent roll and tax returns to verify

accuracy.

8. Copies of All Existing Leases

Every executed

lease is reviewed to assess tenant quality, rollover risk, and whether

lease terms support the income assumptions in the appraisal.

9. Phase I Environmental Site Assessment

A

Phase I ESA identifies potential environmental contamination on or near

the property. If it flags recognized environmental conditions, a Phase

II assessment with soil or groundwater testing may follow. Environmental

risk is a dealbreaker because contamination can destroy collateral

value.

10. Property Condition Report (PCR)

An engineering

firm inspects the roof, HVAC, plumbing, electrical systems, and

structural elements. The PCR quantifies deferred maintenance and

estimates the cost of necessary capital improvements over the loan term.

11. Survey and Title Commitment

An

ALTA/NSPS survey shows property boundaries, easements, and

encroachments. The title commitment from a title company confirms

ownership, existing liens, and any exceptions that must be resolved

before closing.

12. Zoning Compliance Letter or Certificate of Occupancy

Verifies

that the property's current use conforms to local zoning ordinances. A

non-conforming use can impair collateral value if the building is

destroyed and cannot be rebuilt.

13. Insurance Certificates

Proof

of property insurance, general liability, and—where applicable—flood,

earthquake, or environmental liability coverage. Policies must name the

lender as an additional insured or loss payee.

Category 3 — Sponsor & Financial Documents

Even

though the loan is non-recourse, lenders still underwrite the sponsor.

They need confidence that the person or group controlling the property

has the experience and liquidity to manage the asset well and avoid

triggering bad-boy carve-outs.

14. Personal Financial Statement (PFS)

A

current PFS for each key principal, listing assets, liabilities, and

net worth. Lenders typically require sponsors to demonstrate significant

liquidity—often six to twelve months of debt service in liquid

reserves.

15. Three Years of Personal and Business Tax Returns

Tax

returns verify income, confirm the accuracy of the personal financial

statement, and reveal any hidden liabilities or loss carryforwards.

16. Schedule of Real Estate Owned (REO)

A

detailed listing of every property the sponsor owns, including address,

property type, current loan balance, NOI, and vacancy rate. This shows

the lender how experienced the sponsor is and whether they are

overleveraged.

17. Résumé of Real Estate Experience

A

narrative or formatted CV documenting the sponsor's track record in

acquiring, operating, and disposing of similar property types.

Non-recourse lenders place heavy weight on relevant experience—a

first-time investor is unlikely to qualify without a co-sponsor.

18. Credit Authorization and Background Check Consent

While

non-recourse loans do not typically appear as personal contingent

liabilities on credit reports, lenders still pull credit to check for

bankruptcies, judgments, or derogatory marks that signal risk.

Category 4 — Closing & Post-Closing Documents

These

are the legal instruments that formalize the loan and create the

lender's security interest in the property. Many are drafted by the

lender's counsel, but the borrower must review, negotiate, and execute

them.

19. Promissory Note

The note specifies the loan

amount, interest rate, payment schedule, maturity date, and any

prepayment provisions including yield maintenance or defeasance

requirements.

20. Mortgage or Deed of Trust

This

instrument grants the lender a lien on the property. It is recorded in

the local land records office, providing public notice of the lender's

security interest.

21. Assignment of Leases and Rents

Assigns

the property's rental income to the lender as additional collateral. If

the borrower defaults, the lender can intercept rent payments directly

from tenants.

22. Environmental Indemnity Agreement

Regardless

of the non-recourse structure, nearly all lenders require an

environmental indemnity that survives foreclosure. This indemnity

typically is recourse—meaning the sponsor is personally liable for remediation costs if contamination is discovered.

23. UCC Financing Statements

Uniform

Commercial Code filings perfect the lender's security interest in

personal property associated with the real estate—fixtures, equipment,

and receivables.

24. Subordination, Non-Disturbance, and Attornment (SNDA) Agreements

These

three-party agreements between the lender, borrower, and major tenants

ensure that existing leases survive a foreclosure, protecting the income

stream that secures the loan.

25. Estoppel Certificates

Signed

statements from tenants confirming lease terms, rent amounts, and that

the landlord is not in default. Lenders rely on these to validate the

rent roll at closing.

The Carve-Out Guaranty: The Document That Can Undo Non-Recourse Protection

No discussion of non-recourse loan documents is complete without addressing the non-recourse carve-out guaranty,

sometimes called the "bad boy guaranty." This single document is

arguably the most important in the entire package because it defines

exactly when your personal liability shield disappears.

Almost all

institutional lenders require a creditworthy individual—usually the

controlling principal of the borrowing entity—to sign this guaranty. It

creates personal liability for specific "bad acts" that could harm the

lender's collateral position.

Common Triggers That Activate Full Recourse

Filing for voluntary bankruptcy or colluding in an involuntary filing

Fraud or intentional misrepresentation during the loan application

Unauthorized transfer of the property or ownership interests

Common Triggers That Create Loss-Based Liability

Misappropriation of rents, security deposits, or insurance proceeds

Failure to pay property taxes resulting in tax liens

Failure to maintain required insurance coverage

Environmental contamination or waste of the property

Refusing to permit lender property inspections

The critical distinction is whether a violation makes the guarantor liable for the lender's actual losses or for the entire outstanding loan balance.

Some lender forms list as few as three or four trigger acts, while

others list fifteen to twenty. Always have your attorney review and

negotiate this document before signing.

Practical Tips for Assembling Your Package

Start the SPE before you find the property.

Formation documents take time to prepare correctly, especially

bankruptcy-remote provisions. Having the entity ready eliminates weeks

of delay.

Order the Phase I ESA and appraisal early.

These are the two longest lead-time items, often requiring four to six

weeks. Environmental surprises discovered late can kill a deal.

Keep a living rent roll. Update it monthly. Lenders will ask for a current version at application, again during underwriting, and once more at closing.

Pre-draft estoppel certificates and SNDA agreements.

Getting tenant signatures takes longer than borrowers expect,

especially with national credit tenants whose legal teams have their own

review cycles.

Maintain a digital document room.

Organize files by the four categories outlined above. Underwriters who

can find what they need quickly are more likely to issue favorable

terms.

Negotiate the carve-out guaranty as aggressively as the interest rate.

Request cure periods for operational carve-outs like tax payments or

inspections, and push for loss-based (rather than full-balance)

liability wherever possible.

How Lendersa Helps You Navigate Documentation

Preparing

a non-recourse document package can feel overwhelming, especially when

different lenders—CMBS conduits, life insurance companies, private

lenders—each have variations on what they expect. Lendersa

simplifies this by letting you submit your deal once and receive

competing offers from multiple lenders. The platform's AI matching

engine identifies which lenders are the best fit for your property type,

loan size, and experience level—so you spend time preparing documents

for lenders who are genuinely interested in your deal, not chasing dead

ends.

Whether you are financing a stabilized multifamily asset, a

retail center, or an industrial property, Lendersa connects you with

conventional and hard money lenders who offer non-recourse structures.

You can start comparing options without providing a Social Security

number, which means you can gauge your document requirements before

committing to a full application.

Frequently Asked Questions

What is a non-recourse commercial real estate loan?

A

non-recourse commercial real estate loan is a secured loan where the

lender's recovery in the event of default is limited to the collateral

property. The lender cannot pursue the borrower's personal assets, bank

accounts, or other properties to cover a shortfall.

Do I still need to provide personal financial information for a non-recourse loan?

Yes.

Even though the loan is non-recourse, lenders still underwrite the

sponsor. They review personal financial statements, tax returns, credit

history, and real estate experience to ensure the borrower can

competently manage the property and is unlikely to trigger carve-out

violations.

What is a bad boy carve-out guaranty?

A bad

boy carve-out guaranty is a document signed by the loan's

guarantor—typically the controlling principal—that creates personal

liability for specific misconduct such as fraud, voluntary bankruptcy,

misappropriation of rents, or failure to maintain insurance. It is

standard on virtually all non-recourse commercial loans.

How long does it take to close a non-recourse commercial real estate loan?

Non-recourse

commercial real estate loans typically take 45 to 90 days to close,

compared to 30 to 60 days for conventional recourse commercial loans.

The additional time reflects more extensive underwriting, environmental

assessments, and SPE documentation requirements.

What is a Single Purpose Entity and why is it required?

A

Single Purpose Entity (SPE) is an LLC or corporation formed solely to

own the collateral property. Lenders require SPEs to isolate the asset

from the borrower's other business activities and debts, making it

harder for the entity to be pulled into an unrelated bankruptcy

proceeding.

Can a non-recourse loan become a recourse loan?

Yes.

If the borrower or guarantor violates any of the carve-out

provisions—such as committing fraud, filing for voluntary bankruptcy, or

misappropriating property income—the non-recourse protection can be

partially or fully stripped away, making the guarantor personally

liable.

What minimum property qualifications are needed for non-recourse financing?

Most

non-recourse lenders require a DSCR of at least 1.25x, an LTV between

65% and 75%, and a stabilized, income-producing property. Class A or

strong Class B assets in major metropolitan areas are preferred.

How can Lendersa help me find a non-recourse lender?

Lendersa

is an AI-powered loan marketplace that matches your deal with competing

lenders. You enter your property details once and receive offers from

conventional and hard money lenders offering non-recourse structures—no

SSN required to start comparing.

Key Takeaways

Non-recourse

CRE loans require documents across four categories: entity structure,

property asset, sponsor financial, and closing legal instruments.

A Single Purpose Entity with bankruptcy-remote provisions is a baseline requirement for nearly all non-recourse lenders.

The carve-out guaranty is the single most consequential document—it defines when your non-recourse protection disappears.

Environmental indemnity is almost always carved out as a recourse obligation, even on otherwise non-recourse loans.

Closing timelines run 45–90 days, so order long-lead items like Phase I ESAs and appraisals immediately.

Lendersa lets you compare non-recourse loan offers from multiple lenders with one submission, streamlining the process.